Estate Planning

Over half of Americans (51-55%) die with no estate planning.

Most common excuses?

- Not necessary (18%)

- Too complicated (16%)

- Too expensive (14%)

- Belief that the spouse and children will

- automatically receive assets (13%)

Will & Estate Planning Lawyers in Syracuse NY

Estate planning consists of much more than planning for distribution of assets after death. Estate planning starts with life planning. The first object of estate planning is providing for yourself through the rest of your life.

While a will or trust is the cornerstone of any plan, a comprehensive estate plan includes planning for illness and physical or mental incapacity. Arrangements may include: using a power of attorney to designate someone to handle your financial affairs, designating a health care proxy to make decisions regarding your medical treatment and act as patient advocate if you are unable to do so, or identifying a guardian for your minor children so that the decision is not left to a stranger.

It is never too early, or too late, to address your estate plan. The estate planning attorneys at Melvin & Melvin, PLLC will work with you to develop a plan appropriate to your situation. We will help you to maintain your family’s financial security by building a plan around your unique needs and circumstances, whether your concern is passing your home to your children, providing for a child with special needs, or minimizing estate taxes.

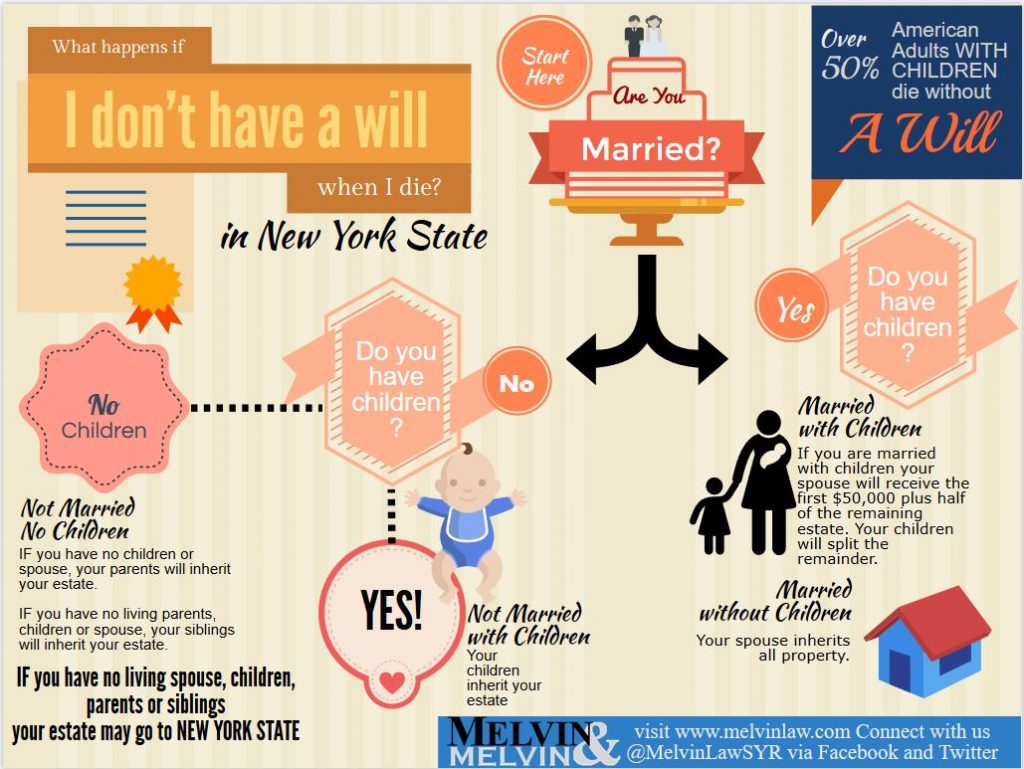

What happens if I die without a will?

Your estate contains everything you owned, with a few exceptions. Whether or not the state’s plan corresponds with your wishes, the administrator of your estate must distribute everything in your estate to those people named in the statute, New York’s intestacy statute ([EPTL Article 4]).

The statute starts with your spouse, if you have one, and your issue, if you have any. One’s issue is descendants in any degree (children, grandchildren, great-grandchildren, etc.) including adopted children. If you have no issue, then the statute looks further up your family tree until there is a group of living relatives, who will receive the property in your estate.

- If you are married and have no issue, then your spouse receives your entire estate.

- If you are married and have children, then your spouse receives $50,000 and one-half of the remaining property in the estate. The children receive the remaining estate property, in equal shares. If any of the children are deceased, then their children, if any, receive their parent’s share.

- If you are not married or your spouse has not survived you and you have issue who survive you, then your issue will receive all the property in the estate, in equal shares, by representation. Representation is a method of dividing property so that it is split equally between each member of a generation eligible to receive it. If all of your children are still living, they split the estate equally. If one or more of your children died before you, the shares for all of your children who have issue are combined. That combined share is split equally between their children.

- If you have no surviving spouse or issue, but you have one or more living parents, then your parents receive your estate.

- If you have no parents, issue or spouse surviving you, then any living siblings will receive your estate in equal shares.

- If you have no parents, siblings, issue or spouse who survive you, then your property is shared between living grandparents, or if you have no living grandparents, then their issue out to first cousins.

- If there is no one in the above list, but there are great-grandchildren of your grandparents living, they receive the estate property.

- If there is no one in the above list, then the State of New York receives your property.

Do I need a will?

If you are happy with the distribution plan in the intestacy statute, then perhaps not.

However, if your situation calls for something different, then you need a will. If, for example, you have young children, you may want to suggest a guardian for the children if needed. Or you may want to leave your estate in trust for the children, so you can name the trustee and specify under what conditions the children receive the property. Or you may want to ensure that your spouse receives the entire estate instead of possibly splitting it with the children. You may want to leave a gift to charity. Or, if your estate may be subject to the federal or state estate tax, you may want to engage in tax planning.

In all of these cases, or any other in which you wish to change the default distribution, you will need a will or a revocable trust.

Wills, Revocable Trusts, and Other Planning Tools

The primary consideration in estate planning is providing for you and your loved ones. Secondary considerations can include tax planning, making sure a prized family heirloom stays in the family, or something else. Wills, revocable trusts, retirement accounts, joint tenancies and other devices are not an end in themselves. They are tools to accomplish your plans.

Health Care Proxies and Powers-of-Attorney

If something happens to you that are unable to make your own decisions, someone will have to be appointed by the court to act in your place, unless you have provided for someone to act for you. A health care proxy tells your medical providers who is authorized to make decisions for you when you are unable, allowing your loved ones to act quickly in a crisis to make decisions as you would want them made. A power-of-attorney allows your loved ones to act as your financial guardian when you are unable to make your own financial decisions or to assist you even when you are still able.

Wills

A will is your final direction of what you want to happen to all of your property once you die. A will overrides the intestacy statute, instead providing for your loved ones as you see fit. Although an important part, a will should be part of a larger plan including a health care proxy, power-of-attorney, and non-probate assets.

Irrevocable Trusts

An irrevocable trust is a gift that splits ownership into two parts: legal and beneficial ownership. The creation of a trust gives legal title to the trustee and beneficial ownership to the trust’s beneficiaries. The trustee owns the property but administers it for the benefit of the beneficiaries based on the purpose of the trust and directions of the trust document.

A trust can be created during life (a lifetime trust) or under a will (a testamentary trust). An irrevocable trust is a gift. Once created, it cannot be revoked or taken back. Generally, an irrevocable trust will also be set up such that it cannot be modified.

Trusts can be used to accomplish many goals. They can be used to provide liquid assets for administering an estate that is largely made up of non-cash assets like real property or business interests. They can be used to give gifts to charity, to provide an income stream back to the creator or pass assets to children or others outside of the estate and gift taxes. They can be used to minimize estate or gift tax burdens.

Trusts can also be used to structure a gift or legacy to a person. Instead of receiving a large amount of property outright, it can be administered in a way that’s tailored to the recipient. They are often used when giving gifts to a minor, someone with special needs, someone who does not manage money well, or someone with a different, unique, situation where an outright gift is not desirable or practical.

Revocable Trusts

A revocable trust is a trust that the creator can alter or revoke at will. The creator of a revocable trust is accountable only to himself while he or she is the trustee and can deal with the assets as if they did not belong to the trust. If the creator becomes incapacitated, then a successor trustee can step in to take care of the property. After the creator’s death, the trust becomes irrevocable and all property in the trust passes to the beneficiaries outside of probate.

Revocable trusts can be a useful tool for handling particular assets, for privacy, or for avoiding the probate process. However, there are several pitfalls, and there are often other ways to accomplish the same goals. In many parts of the state, the probate process is not any more cumbersome than administering a trust, and can cost less. Non-probate assets can be used to keep a large portion of the estate out of probate at less cost. And a power-of-attorney can be used to ensure someone can step in to make financial decisions when needed. Titling mistakes or omissions can mean that assets pass through probate anyway. They can also lead to litigation and other problems. And finally, because they don’t need to be approved by the Surrogate’s Court, revocable trusts offer less protection against undue influence, forgery, and similar problems than the laws governing wills.

Non-Probate Assets

Non-probate assets are any property that passes to another person outside of the probate process or under the intestacy statute. This property includes assets in a trust and assets such as life insurance or retirement accounts that pass via a beneficiary designation. If beneficiaries are not designated properly, however, those assets can end up in the estate and pass through probate. Non-probate assets also include property that is jointly-titled with a right of survivorship, which can include real property, vehicles, or bank accounts. Assets that are jointly-owned with a right of survivorship automatically pass to the other owner upon one owner’s death.

A strategic use of such assets can result in the bulk of one’s property being distributed outside of probate without the extra expense and administration of a revocable trust.

Protections for the Family

As a general rule, a person can leave a will that distributes his or her property in whatever manner he or she wishes. There are, however, two exceptions: the family exclusion and the elective share.

The Family Exclusion

The family exemption is a set of specific property that is set off from the estate and immediately becomes the property of the deceased’s surviving spouse, if there is one, or all children under the age of twenty-one. The set of property under the family exclusion is not part of the estate. Even if it is distributed by the will, the surviving spouse (or children under twenty-one if there no surviving spouse) may still take the property. For a list of property included, see [What is a deceased person’s estate?]

The Elective Share

In New York, a surviving spouse has the right to elect to take a specified share of the deceased’s estate, even if contrary to the deceased’s stated wishes.

The specified share, called the elective share, is the greater of $50,000 or one-third of the net estate. In the event that a spouse is left less than this under the deceased’s will, he or she may make the election and receive the elective share before anything is distributed to those named in the will.

For purposes of the elective share only, the estate also includes most non-probate transfers including:

- Death-bed gifts

- Certain transfers for less than fair-market value within one year of death

- Joint bank accounts

- Transfer-on-death accounts

- Jointly-owned real property

- Certain transfers to trusts

- Retirement accounts, pensions, and similar

- General powers of appointment

The elective share is reduced by any amounts given to the surviving spouse under the will or by non-probate transfer.

Disinheritance

Except as detailed above, a person can disinherit anyone he or she chooses. Children can be completely disinherited unless they are under twenty-one and the deceased does not have a surviving spouse. A spouse cannot be disinherited in New York unless he or she waives the right to the elective share and the family exclusion in a written agreement. In the event that you wish to disinherit a relative, you should have a will or trust drawn up to accomplish that purpose.

Same-sex Marriages

In New York, same-sex married couples have the same rights as opposite-sex married couples. Sometimes, however, their situation can be more complicated. Same-sex married couples generally, but not always, have the same rights and benefits as opposite-sex married coupled under federal law. New York recognizes same-sex marriages from other states and countries, but does not recognize civil unions or similar arrangements as a marriage. If one person in such an arrangement dies as a citizen of New York, his or her partner will not be recognized as a family member and will have no rights to the other partner’s estate without proper planning.

Common-Law Marriages and Unmarried Couples

New York does not recognize common-law marriage. In some situations, New York may recognize marital rights under a common-law marriage entered into in another state. Under New York law, unmarried couples have no family rights under the laws governing estates. If one member of such a couple dies, the other has no right to any part of the estate, or to be appointed personal representative, without proper planning. Legally, the other person is considered a stranger. Additionally, the other person has no right to be involved in medical or other decisions without a health care proxy or power-of-attorney in place.

Melvin & Melvin has the Syracuse estate planning lawyers who can help you by answering questions and addressing your concerns. If you have any questions or concerns, feel free to email us at [email protected] or call at (315) 422-1311.